Hello,

I need help as i just can’t get my head around how to do this properly.

We trade in goods and some suppliers give us a no-warranty discount on purchase prices ( to cover up costs of potential warranty claims)

I don’t want this discount to diminish the inventory cost the item is held at, but to be held as a sort of buffer account against which i would charge potential warranty claims.

EXAMPLE

We buy 10pcs for 100€ each and get a 50€ discount for warranty claims

I would enter the items at their real purchase price (ie 100€) to get a right inventory cost (and right COGS deduction after sales). But i need to deduct the 50€ discount form purchase invoice to get the right invoiced amount.

Any advice on how to handle this would be appreciated.

You have to understand the bottom line. The bottom line is that, this is a discount. This is a discount because the amount allowed as discount is permanent, if no negative eventualities happen the discount will still be there.

Even though suppliers may open a liability account to handle warranties, no customer opens an asset account to handle warranties receivable unless a claim has been processed and the warranty due for payment. Because of prudence concept.

You can do this anyway.

Select the inventory line on the purchase invoice and enter 100 Euros as the rate.

Add another line and enter the total no warranty discount amount there but in negative. Select some revenue account there.

The inventory will be valued at 100 Euros per unit and the no warranty discount will end up as income in some other account. This is the best solution I have if you really want to maintain the price/cost of the inventory at 100 euros. Because in your case the warranty received is an income. Account payable will be 50 Euros too. Perfect

I agree with @Abeiku’s initial point. In the situation described, you have been given a permanent discount. That discount should be reflected in the cost of inventory, because no matter what happens in the future you have paid less for the goods.

Allocating the discount to an income account by entering a negative line item will balance your books. But it will also do two undesirable things:

Add to your current taxable income. Although an offsetting reduction will eventually occur when the goods are sold, you might keep slow-moving items in inventory for years. Meanwhile, you will have paid tax on the income you did not yet receive. And later, you will claim a deduction for an expense you did not really incur.

Add to the current value of Inventory on hand. This overstates your current assets. As mentioned above, this overvaluation is what will eventually (hopefully) give you a larger cost of goods expense. But until that happens, you will be misrepresenting your position on your balance sheet. Auditors will not like this. Bankers will not like this. And, in some jurisdictions, inventory on hand is taxable every year as a property tax, so you will not like this.

As @Abeiku wrote, normal accounting practice does not build warranty allowances into assets. It considers potential warranty costs when setting profit margins, then records warranty costs as current expenses. So in your example, the question you should be asking is how much margin do you need to add to the €50 cost when setting your sales price. If there is a 10% chance you will have to replace the item under warranty, add €5 plus your desired profit. If there is a 50% chance, add €25 plus desired profit. Any future warranty costs can then be posted to a current expense account, reducing profit and net income in the period when they occur.

One other thing you might consider is transferring some of your current net profit from Retained earnings to a warranty reserve equity account for visibility. But, understand that this would really just be a subdivision of Retained earnings.

Thank you for all your answers!

And yes, this is actually accounting issue, so not really related to Manager.io functionality.

I consulted with local accounting and tax consultant and we did the following:

We created a LIABILITY account called “Long term reservations for warranty claims”, and we are crediting that account with given discounts.

If we incure a warranty cost the account will be debited by that amount and the corresponding expense account “Waranty claims expenses” is credited.

At the end of the accounting year some part of the Reservations must be shown as Income ( according to Tax on profit laws) so we’ll adjust accordingly.

@johnny - I whole heartily agree with your consultants - the creation of the liability account.

Except I would simplify the account name to - Provision for Warranty Claims.

That is because, by accepting the discount you are assuming the “liability” for the warranty claims.

As with any other accounting provisions (reservations), annual leave, long service leave, this particular provision will be annually reviewed based on sales, unexpired warranty period and warranty claims received. Also, as with all accounting provisions the movement in the account’s balances will be adjusted accordingly on the tax return as “timing differences”.

I applaud your consultants for their professional recommendation. Far to frequently, people attempt to make their accounting (Manager) accounts exactly the same as their taxation accounts - when often they aren’t . That is why tax returns are a transition document - they start with the accounting profit and end up with the taxation profit.

Exactly, we are making provisions (reservations) for possible future liability. Thank you for further clarifying the point!

As for the account name, i literally translated from our native (Croatian) language name for the account. “Provision for Warranty Claims” will probably be the proper name for English speaking countries ( I’m not a native speaker)

To expand on your comment about taxation.

There is always difference between “Accounting profit/loss” and “Taxation profit/loss”.

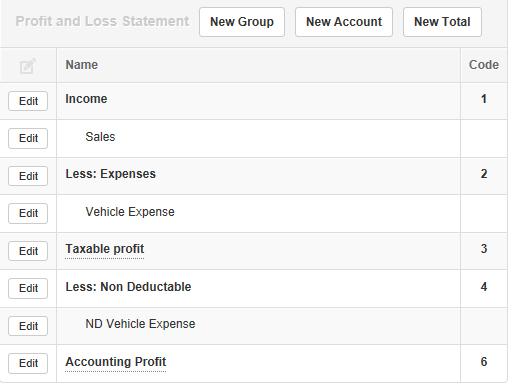

There are lot of examples ( depending on taxation laws in particular country). For example we can only deduct 50% of expenses for personal cars owned by company as tax deductible expense.

In Manager we make two separate accounts for each such item so we can separate tax deductible from non-deductible expenses.

So it’s quite easy to make required Profit tax statement from Manager books.

I don’t know if there is some why to make the report automatic from Manager…

No, there is not. You have the choice of splitting the asset (the way you are now doing) so the financial statements automatically show the 50% deductible and non-deductible portions or leaving them together and calculating the split when filing tax returns.

In my personal experience, I believe the second approach is more common. This would normally be just one more among several differences between financial and tax accounting. But there is certainly nothing wrong with doing things the way you are. Be careful, however, that you are not giving up potential tax benefits by only reporting the split. (There may be aspects of your tax laws that make it beneficial to report the full amounts in some places, even though only 50% can be shown in others.

@johnny, note that the totals added in the preceding example are for display purposes only. They are not technically accounts. That means they have no underlying transactions of their own, but only report the summation of group totals higher up in the chart of accounts.

As a consequence, you will not be able to drill down on them from the Summary page or Profit and Loss Statement to see what makes them up. But they may be all you need. And, of course, access to relevant transactions would still be available by drilling down on Vehicle Expense and ND Vehicle Expense accounts.