The Federal Board of Revenue (FBR) of Pakistan is set to implement a digital invoicing system in the near future, which will be directly integrated with FBR. The official details can be found in the following document:

This update is highly relevant for businesses operating in Pakistan and using Manager for their accounting and invoicing needs. It would be in the best interest of Pakistani users if Manager could adopt these regulations in a timely manner, ensuring seamless compliance with FBR’s new requirements.

Early adoption of this system within Manager would not only help businesses stay compliant but also streamline tax reporting and digital invoicing processes. I encourage the developers to review the new rules and consider incorporating the necessary updates.

Looking forward to feedback from the community and developers on this matter.

Thanks for sharing this important update. The integration of the FBR Digital Invoicing System is crucial for businesses in Pakistan to ensure compliance. Implementing this within Manager would greatly benefit users by simplifying tax reporting and automating invoicing.

It would be helpful if the developers could review SRO 69(I)/2025 and provide insights on potential implementation timelines. Early adoption would ensure a seamless transition and prevent compliance issues.

Looking forward to hearing thoughts from both the community and the development team!

@lubos Any update on this?

its important, deadline is 31 june, if there is no solution provided, people have to switch to some other software which allows integration with FBR

yes i already received email about this after 30 june there will be fine. iam right now working on custom solutions. but iam afraid we wil have to leave manager for that.

Manager will provide support to all localities provided official documentation exists and provided enough time. In this case, the api was only fully released beginning of this month and this gives the developer 30 days to develop a full working solution.

I think we have to be a bit realistic with our time expectations, especially since there’s been no initial localization for Pakistan except for Currency. So the start will have to be from dead scratch, unfortunately.

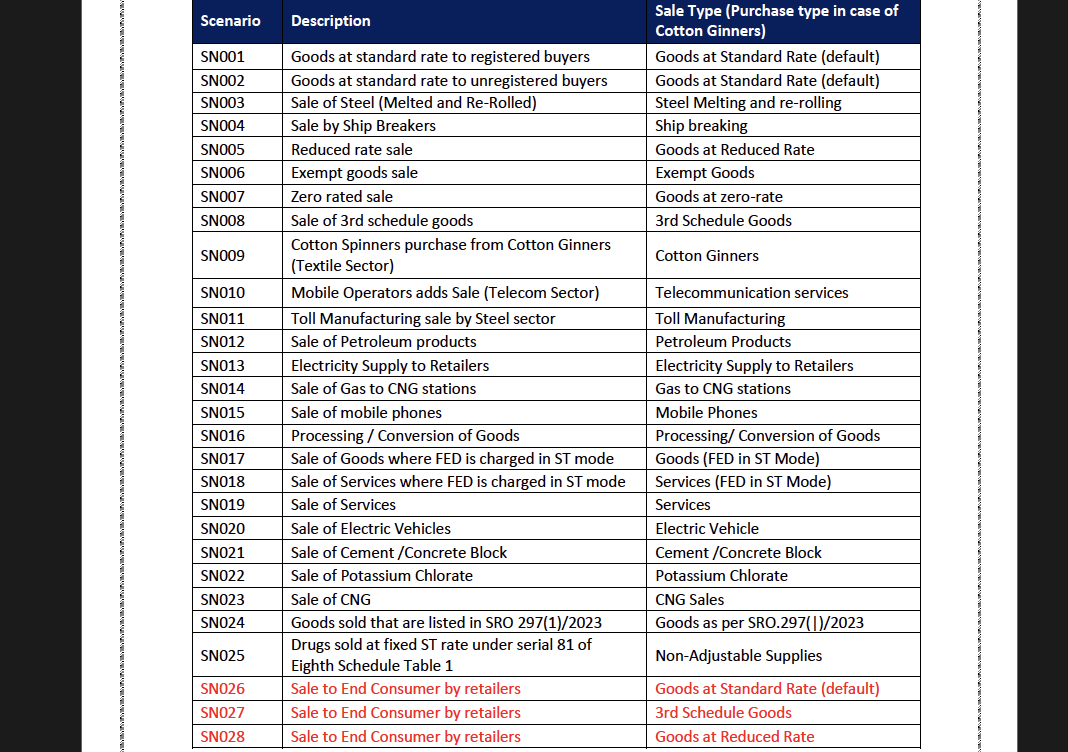

I will start with creating the necessary Custom Fields for Pakistan based on the requirements in this document:

And just in case, this post ever gets overlooked, I’m going to categorize it in ideas

I apologize again for any inconvenience users may have to experience until this gets done.

Also, regarding “salesTaxWithheldAtSource”, does this apply for specific items only? What’s the general idea behind having withhled tax at line level here?

Also also, is “saleType” equivalent to Tax Code, since the example used this value:

@Ealfardan Thank you very much for your reply to this post, we are not seeing much interest in this matter from our side, and obviously the team needs time for this work. Once again, thank you very much for your positive reply.

Here’s an explanation, drawing on current practices and regulations by the Federal Board of Revenue (FBR):

Extra Tax (in Pakistan)

As mentioned before, “extra tax” isn’t a formal, standalone tax category in Pakistan’s tax laws. However, it can refer to several scenarios where additional tax liabilities or charges are imposed beyond the standard rates:

Surcharges and Regulatory Duties: The FBR often uses Statutory Regulatory Orders (SROs) to impose additional duties or surcharges on imports and sometimes on domestic supplies. These are officially known as Regulatory Duties (RDs) or Additional Customs Duties (ACDs). They function as an “extra tax” on specific goods to regulate trade, protect local industries, or simply to generate more revenue. For example, SROs are frequently issued to levy RDs on luxury items or goods where the government wants to discourage imports.

Increased Tax Rates: When the government, through a Finance Act, increases the rate of an existing tax (like sales tax or income tax), the incremental amount paid by taxpayers is colloquially referred to as “extra tax.”

Penalties and Default Surcharges: If a taxpayer defaults on their tax obligations, such as late filing or non-payment, the FBR can impose penalties and surcharges. These are “extra” amounts the taxpayer has to pay due to non-compliance.

Withholding Tax for Non-Filers: In Pakistan, non-filers of income tax returns often face higher withholding tax rates on various transactions (e.g., bank interest, property transactions, vehicle purchases). This higher rate acts as an “extra tax” to incentivize taxpayers to file their returns and become part of the active taxpayer list.

Further Tax (in Pakistan)

Further Tax is a well-defined concept in Pakistan’s sales tax regime, governed by the Sales Tax Act, 1990.

Purpose: It is levied on supplies of taxable goods made by a registered person (for sales tax purposes) to an unregistered person or a person who is registered but not an “active taxpayer” (as per the Active Taxpayers List maintained by FBR). The primary objective of further tax is to promote documentation of the economy and incentivize businesses to register for sales tax.

Current Rate: As per the Finance Act, 2023, the rate of further tax is 4% of the value of supplies. It’s important to note that this is in addition to the standard sales tax rate (which is generally 18% in Pakistan).

Exemptions: There are specific exemptions from further tax, which are often outlined in SROs or the Sales Tax Act’s schedules. These can include:

Supplies of goods already exempt from sales tax.

Supplies to certain types of consumers (e.g., domestic consumers for electricity or natural gas).

Specific goods mentioned in relevant SROs.

Goods listed in the Third Schedule of the Sales Tax Act, where tax is levied on the printed retail price.

Recent Developments: There have been discussions and proposals, particularly in the context of the upcoming budget (FY 2025-26), to potentially abolish further sales tax on unregistered taxpayers. The stated aim is to encourage the registration of the entire supply chain and expand the tax net, even if it leads to a short-term revenue loss for the FBR.

SRO Schedule No. and SRO Item Serial No. (in Pakistan)

These terms are crucial for navigating the specifics of Statutory Regulatory Orders (SROs) issued by the FBR and other government bodies in Pakistan.

SRO (Statutory Regulatory Order): An SRO is a legal instrument issued by the executive branch (like the FBR) under powers granted by an Act of Parliament (e.g., Sales Tax Act, Customs Act, Income Tax Ordinance). SROs are used to:

Provide detailed rules, procedures, and conditions for implementing the main tax laws.

Grant exemptions, concessions, or reductions in duties/taxes for specific goods, services, or sectors.

Impose new duties (like Regulatory Duties) or modify existing ones.

Clarify ambiguities or address practical issues arising from tax laws.

They are published in the official gazette and carry the force of law.

SRO Schedule No.: Many SROs, especially those dealing with exemptions, concessions, or rates for a large number of items, are structured with various “Schedules.” Each schedule groups similar items or categories. The “SRO Schedule No.” refers to a specific section or list within that SRO. For example, an SRO granting sales tax exemptions might have different schedules for industrial machinery, agricultural inputs, or essential food items.

SRO Item Serial No.: Within each schedule of an SRO, individual goods, services, or conditions are listed, and each is assigned a unique “Item Serial No.” This serial number provides a precise reference point for identifying the specific item or provision covered by that SRO. When taxpayers or customs officials refer to an SRO, they often cite the SRO number, followed by the relevant schedule number and item serial number to pinpoint the exact clause applicable to a particular product or transaction.

You can find SROs on the official FBR website (fbr.gov.pk) by department (Customs, Sales Tax, Income Tax, Federal Excise).

FED Payable (in Pakistan)

FED stands for Federal Excise Duty. It is an indirect tax levied by the Federal Government of Pakistan on the manufacture or production of certain goods, the import of specific goods, and the rendering of certain services.

Scope: Unlike sales tax, which applies generally to all goods and services unless specifically exempted, FED applies only to a selective list of goods and services. This list is primarily found in the First Schedule of the Federal Excise Act, 2005. Common examples include tobacco products, aerated water, cement, certain petroleum products, and certain services like air travel and financial services.

Calculation Basis: The FED can be calculated in several ways:

Ad valorem: A percentage of the value of the goods or services.

Specific Rate: A fixed amount per unit of quantity (e.g., per kilogram, per liter, per stick of cigarette).

Retail Price: For certain goods, FED is levied on the printed retail price.

FED Payable: This refers to the total amount of Federal Excise Duty that a manufacturer, importer, or service provider is liable to pay to the FBR for a specific tax period (usually a month).

Input Tax Adjustment: Like sales tax, the Federal Excise Act allows registered persons to adjust the FED paid on raw materials and inputs used in the manufacture of excisable goods against the FED payable on the final product. This mechanism helps avoid cascading effects of taxes.

Payment Due Date: FED is generally payable by the 15th of the month following the month in which the clearances of excisable goods were made or services were rendered.

Understanding FED payable involves knowing the specific goods/services your business deals with, their applicable rates (as per the First Schedule of the Federal Excise Act, 2005, and any relevant SROs), and the rules for input tax adjustment.