If I understand you correctly, you would pay the supplier the 75 VAT but can only claim 60 VAT as the offset, therefore the question is - does the 15 differential remain as non claimable VAT in the Tax Payable account or does it get transferred to become a claimable expense item instead ?.

On the assumption that you know of the 80% rebate products when receiving the suppliers invoice and that the non claimable 20% can be expensed then you would do the following:

1 - Create a BS > Liability > VAT Non Claimable account.

2 - Create a P&L > Expense > VAT Expense account

3 - When processing the Purchase Invoice you would add two lines to cater for the 20%

@Abu_Hasan, I don’t think you have explained this completely. In addition to @Brucanna’s question about what happens to the differential, I wonder about the basic circumstances in such a transaction. If a supplier assesses 15% VAT on a purchase you make, that tax must be paid to the authority by someone, either the supplier or you.

The more common situation is that the supplier pays it to the authority and you offset it against taxes you have assessed your customers. In your example: 90-75 = 15.

If you are paying the differential to the authority, that is what is known as Withholding Tax (WT) or Tax Deducted at the Source (TDS), or something similar. The purpose of such arrangements is so the authority receives its money with greater assurance. In this situation, you VAT Payable account would still be 15. But you would have a second account for WT payable.

The reason for two different accounts is that VAT payable represents liability to the authority for money collected from customers on behalf of the authority. WT payable represents money you owe directly to the authority for purchases you have made.

If your situation involves withholding tax, read this Guide: Manager Cloud. The process for purchases is described in the second half of the Guide.

You are right.

৳ 15 is non claimable.

The product is internet bandwidth.

We can’t store it. So, there is a lose if we can’t sell the amount that we purchased.

That’s why we can’t claim 100%. Because we can’t sell 100%.

This is very unusual as there are many businesses who can’t sell 100% yet can claim 100%.

Many food businesses can’t 1) sell 100% of their purchases which also 2) can’t be stored so there is a “loss”. So you have unsold purchased food just like you have unsold purchased bandwidth. Anyhow, if that’s the situation, then that’s the situation.

Well you have to do something with the non claimable 20%, as you can’t leave it in the BS > Tax Payable account. If you are putting into the account from sales a credit of 90 and from purchases a debit of 75 then the account has a credit 15 balance, but if you are paying out 30, then the account ends up with a debit 15 balance. If you do this every month then by the end of the year the account will have a 180 debit balance, which is an asset balance but there is no asset, so it needs to be expensed as it is forgone VAT outset.

Just like an unregistered VAT business, the VAT they pay on purchases is expensed as they can’t claim a refund, therefore the VAT you pay but can’t claim as a refund is also expensed.

No. Nor is there likely to be, because what you refer to would be a percentage calculation on top of a percentage calculation, with results possibly posting to different accounts. That gets fairly messy to implement, especially when many users don’t have visibility into the already complex first-level allocations to built-in control accounts. Putting a second layer on top of that is likely to lead to many misunderstandings. At least when you enter this manually, you would be doing something you designed and understood.

You might experiment with a multi-component custom tax code (in a test company). One component would be the reduced version of the basic VAT rate, allocated to Tax payable. Another would be a 0% component allocated elsewhere.

I have to warn you, though, that I have not thought this through in detail. Nor have I tried it out. I would be interested in the results of an experiment, though.

Of cause the tax summary is not satisfactory because your custom tax code totals 15% (12 + 3), all you have done is allocate that 15% into two separate liability accounts.

However, now that you have gone down the path of a custom tax code you can simplify my earlier solution by modifying your custom tax code “Purchase VAT” to being just a single rate and just keep the 12% tax rate (remove the 3%).

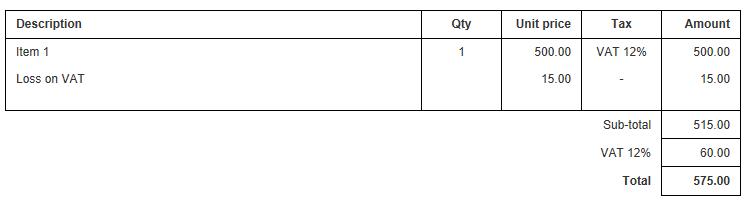

Now on the Purchase Invoice you would select the 12% rate and only 60 would go to the Tax Payable account and the tax report but you will still need to add the line Loss on VAT to take up the expense. Also, you will no longer need that Journal entry

I see two issues with the solution that is emerging:

Your purchase invoice is labelled as having 12% VAT applied. But that is not your rate and may well confuse people. That problem can be solved, if using a custom rate, by giving the tax code another title, such as 80% Factored 15% VAT (that isn’t very elegant, but you get the idea, I hope).

The question first pointed out by @Brucanna remains. Do you know at the time you purchase the bandwidth that you won’t be able to sell it, or is that something that is calculated after the fact? If this is a variable rebate, perhaps it should not be added to a purchase invoice at all, but “given back” via a debit note, entered as a straight line item rather than an applied tax code. Or do you always rebate 20% based on some mandatory assumption that you won’t be able to sell 20% of the bandwidth you purchase?

Bullet point 1 - Code name could be “VAT15% @ 80%” or “Broadband VAT” for clarity.

Bullet point 2 - Mandatory based on the comments “we can only rebate 80% of that 15%” and “৳ 15 (20%) is non claimable”.

The initial question of “remain as non claimable VAT or become a claimable expense” appears to be resolved as “VAT offset forgone”, therefore an expense.

It was not clear to me from @Abu_Hasan’s initial post that the 80% figure was constant from purchase to purchase. It came out later that this was related to unsold bandwidth, which is obviously going to be a variable amount. So my question still seems valid: is the limit always 80% based on some regulation or formula, or can it change?

We can’t claim 100% VAT on Internet Bandwidth.

This is a rule set by the government.

I asked to the officials. They replied, there is a chance of not selling the whole amount.

Internet bandwidth can’t be stored, you know that. This is a possible reason.

Whatever the reason, the rule is, we can claim 80% VAT on Internet Bandwidth.